What is the Bank of England’s base rate?

Anya Gair, Head of Organic

Anya Gair, Head of OrganicChances are, you’ve likely heard the Bank of England’s base rate mentioned in the news - probably in relation to mortgage interest rates or inflation. But what is the base rate, and how does it impact you? Keep reading to find out.

In this guide

- What is the Bank of England’s base rate?

- How does the base rate affect interest rates?

- What is the history of the Bank of England’s base rate?

- What is the current Bank of England base rate?

- Why is the base rate not going down?

- What’s going to happen to my mortgage costs?

- When is the next Bank of England base rate meeting?

- How often does the Bank of England base rate change?

What is the Bank of England Base Rate?

What is the Bank of England’s base rate?

The Bank of England’s base rate, sometimes called the Bank of England rate or simply the base rate, is the rate the Bank of England charges other lenders to borrow money. It’s used by other banks and building societies to set their own interest rates on loans such as mortgages, as well as savings accounts.

Keep an eye on the current Bank of England base rate with our Tracker.

How does the base rate affect interest rates?

When the base rate goes up, this makes borrowing more expensive for lenders, so they often raise their own interest rates in response. This is good news if you’ve got cash in the bank, as you’ll earn more interest on your savings. But it can be bad news if you want to borrow money, as it makes taking out loans for things like mortgages, cars or personal finance more expensive. On the other hand, when the base rate falls, so does the cost of borrowing, so interest rates often tend to follow suit.

See what's happening with live rates and compare mortgage deals with our Mortgage Rate Comparison tool.

Worried about rising mortgage costs?

If you’re a homeowner or you’re thinking of applying for a mortgage, you might be worried about how these changes will impact your finances. Create a free Tembo plan today to see what rates you could be offered and the monthly costs.

What is the history of the Bank of England’s base rate?

The history of the Bank of England’s base rate goes back further than you might think. The base rate was created when the Bank of England was granted a Royal Charter by King William and Queen Mary in 1694. This charter originally stated that the bank was founded to “promote the public Good and Benefit of our People”, which at the time meant funding wars with France.

Over the centuries, the base rate has been used to cool or stimulate the economy or control inflation, in particular during uncertain times such as during wars, financial crises or pandemics.

If you look at how the base rate has changed since it was first introduced, you can see that there were some periods when the base rate stayed stable, and others when it was constantly in flux.

For example, the highest base rate level ever recorded was in 1979 when it peaked at 17%. The lowest ever recorded level was in 2020 when it fell to 0.1% during the Coronavirus pandemic. Typically, a much more normal range for the base rate is between 4-6%.

What is the current Bank of England base rate?

The Bank of England's base rate today is 3.75%. The Bank of England's Monetary Policy Committee (MPC), which sets the base rate, voted to hold the base rate at 3.75% at the last meeting in June 2026. They will next meet on 30th July 2026, to determine whether they will cut the base rate again, hold it at 3.75% or increase it.

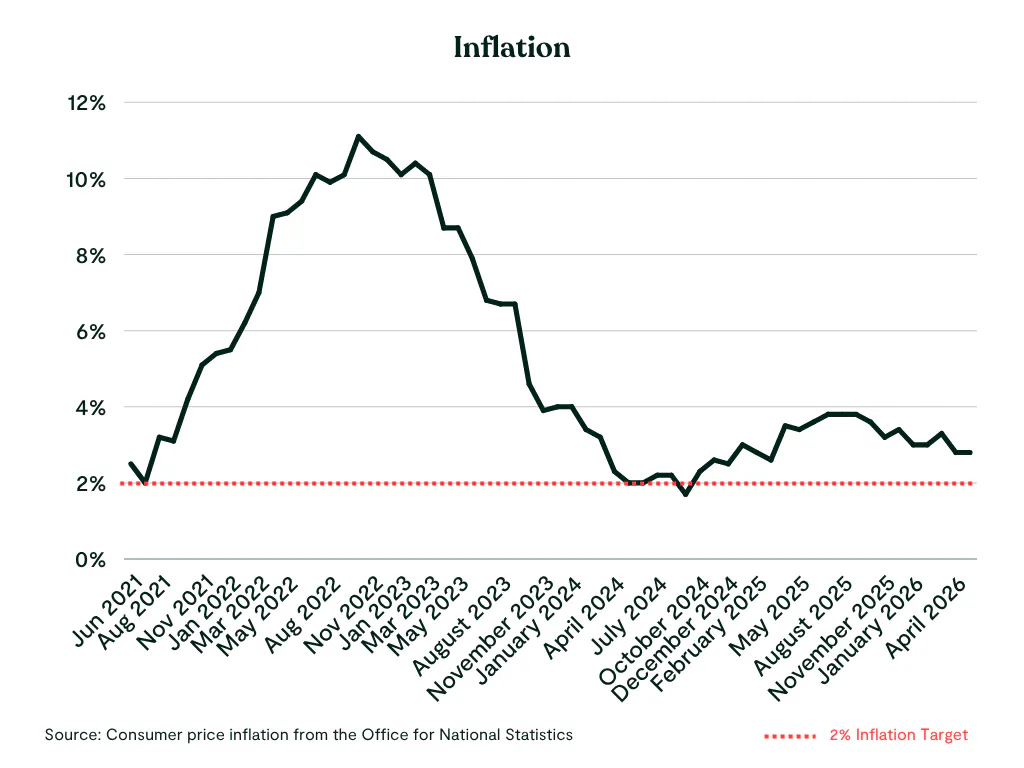

Why is the base rate not going down?

The Bank of England voted to keep the Bank Rate at 3.75% after the latest inflation figures showed that CPI inflation stayed stable at 2.8% in May. It has since fallen again in June to 2.6%, and the unexpected fall was largely driven by lower motor fuel prices.

While inflation has moved closer to the Bank’s 2% target, it still remains above target. As a result, the Bank may choose to keep interest rates on hold while assessing whether inflation will continue to ease. Although markets expect further rate cuts over time, the pace and timing will depend on future inflation and economic data.

Keep reading: Tembo's mortgage rate and house price predictions for 2026

What’s going to happen to my mortgage costs?

If you’ve got a fixed-rate mortgage, you’re protected from interest rate rises until the end of your fixed term. If your fixed rate is set to end in the next six months, it may be wise to speak to a mortgage broker sooner rather than later.

Lenders have rapidly repriced fixed-rate deals off the back of rising inflation fears, so a mortgage rate you had your eye on a month ago may not be available now.

If you’re on a variable rate deal, every time the base rate rises, you will likely see an immediate impact on your monthly repayments.

See what rate you could get now without applying.

Learn more: What should I do when my fixed-rate mortgage ends?

Struggling to remortgage? You're in the right place

Here at Tembo, we can help you find the best rate for you from thousands of mortgage products, including whether it’s worth staying with your current lender.

When is the next Bank of England base rate meeting?

The Bank of England’s next base rate meeting will be held on Thursday 30th July 2026. They usually meet every six weeks, but during times of crisis, they tend to meet more often.

How often does the Bank of England base rate change?

There is no hard and fast rule for how often the Bank of England’s base rate changes. The base rate will only be increased when the central Bank feels it’s necessary to do so. Some years, the base rate stays stable and barely changes, other times, like more recently, the base rate is changed each time the Bank of England meets.

See what you could rates you could be offered today

At Tembo, we’re experts at helping buyers and remortgagers increase their affordability, so you can buy sooner or access lower rates.