What happens to mortgage rates in a recession?

When a recession hits, it can be a worrying time for homeowners with upcoming remortgages, home movers and first-time buyers, particularly those facing tightening budgets, pay cuts or even redundancies. This article explores what happens to mortgage rates in a recession and what homeowners and prospective buyers should consider.

In this guide

- What is a recession?

- What causes a recession?

- What happens during a recession?

- How often do recessions happen?

- Is the UK heading for a recession?

- How long does a recession last?

- How do mortgage rates change in a recession?

- Is a recession good for mortgage rates?

- How does a recession affect my mortgage?

- Should I pay off my mortgage in a recession?

- Do house prices fall in a recession?

- Is it possible to get a mortgage during a recession?

- What happens to savings rates during a recession?

Key takeaways

- Lower interest rates: Mortgage rates typically fall during a recession as the Bank of England lowers the base rate to stimulate spending, although this isn’t guaranteed.

- Fixed vs variable: Tracker and variable-rate mortgages usually get cheaper, while fixed-rate deals remain unchanged until the term ends. See what rate you could get here.

- Stricter lending: Even if rates are lower, banks often tighten their lending criteria, making it harder to be approved for a loan.

- House price impact: Property prices may fall or grow more slowly, which can benefit first-time buyers but challenge those looking to upsize.

- Financial safety: Prioritise an emergency savings fund over mortgage overpayments during a recession to protect against potential income loss.

What is a recession?

In simple terms, a recession happens when a country's economy shrinks significantly over time. Typically, this means the country's gross domestic product (GDP) has been negative for two quarters in a row. Other signs that a country might be heading for a recession are rising levels of unemployment, as well as reduced levels of spending, manufacturing and income.

Find the right deal for you in uncertain times

Whether rates are rising or falling, our award-winning experts can help you secure the best deal for you that works with your finances. Start by discovering your mortgage options.

What causes a recession?

Recessions can stem from different triggers, but they generally happen when something stops the economy from growing or causes it to shrink.

Typical causes of an economic contraction include:

- Economic shocks: Sudden, unexpected events like the COVID-19 pandemic, or the current conflict in the Middle East.

- Excessive debt: High levels of individual or corporate debt that become unsustainable.

- Asset bubbles: Market crashes caused by over-inflated investment prices (e.g., the 2008 housing bubble).

- Price volatility: Extreme levels of either inflation or deflation.

Read more: How to navigate a volatile mortgage market

What happens during a recession?

When a recession hits, the economy struggles, and there is less money circulating. The economic output of a nation slows down as consumers spend less, which means businesses can struggle. The government may also issue tax cuts to help stimulate spending, which means it gets less money from taxes. This can reduce the government spending pot, impacting things like funding for benefits and public spending.

How often do recessions happen?

Recessions are a natural part of economic cycles; economies regularly move through periods of growth and contraction over time. Most people are likely to experience several recessions during their lifetime.

In the UK, the last recession was during the COVID-19 pandemic, when in the first two quarters of 2020 GDP saw negative growth. The UK economy didn’t return to pre-pandemic levels until late 2021.

Before that, the UK experienced a recession in 2008-2009 when a high amount of subprime mortgage deals in the US created a housing bubble. When this bubble popped, the British banking sector and, as a consequence, the UK economy were significantly impacted, resulting in the worst recession in the UK since the Second World War.

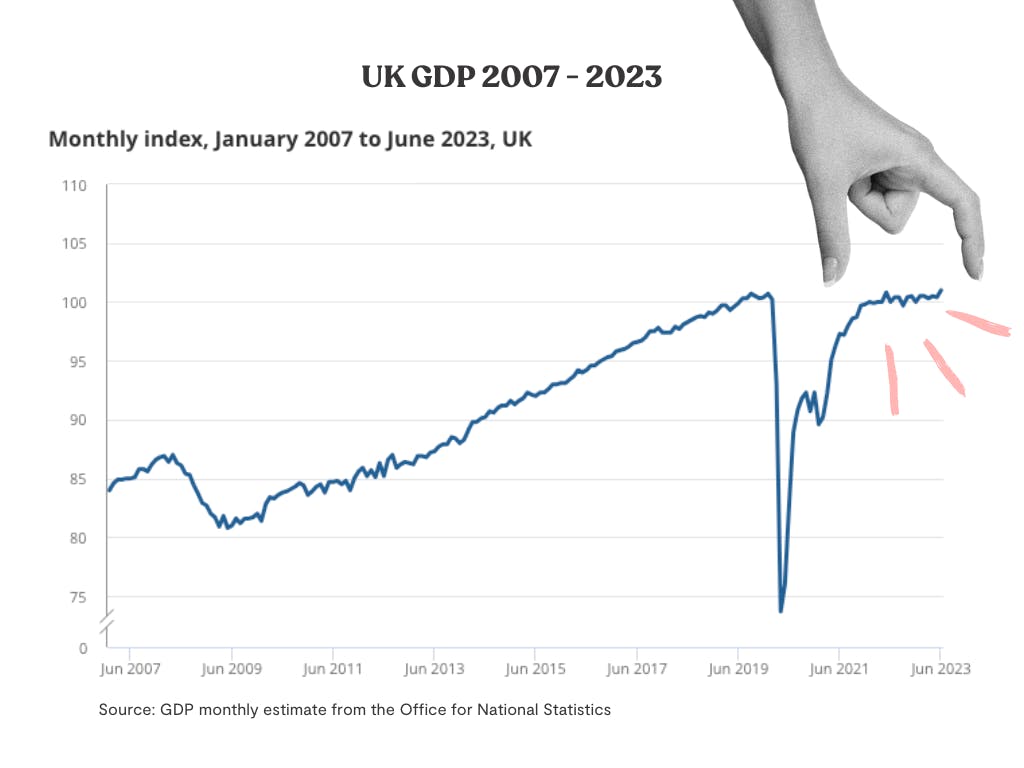

Is the UK heading for a recession?

Right now, whether the UK will go into a recession or not is largely influenced by whether the conflict in the Middle East continues into next year. A prolonged conflict would stunt global growth, which could drive some countries into a recession and cause energy shortages.

According to the latest Economic Outlook by the Organisation for Economic Co-operation and Development, if there is no agreement between the US and Iran until 2027, this could reduce global GDP growth to 2.1% this year, from 3.4% last year.

The latest data shows that GDP grew by 0.6% in the first quarter of 2026, expanding 1.4% on an annual basis when compared to the same period last year. And current forecasts predict that the UK economy will grow by 0.9% this year and 1.1% in 2027, narrowly missing a recession.

That said, the UK economy still faces challenges. The energy shock and instability from the conflict in the Middle East are expected to push inflation higher over the summer months. This has already had an impact on interest rates, with hundreds of lenders repricing deals and raising mortgage rates.

Higher prices and mortgage costs could hit consumer spending, and if they impact economic growth enough, could cause a mild recession. However, all this could change if the conflict in the Middle East is brought to a swift conclusion.

Use our Mortgage Rates Comparison tool to see what's happening to live rates and compare today's best deals.

How long does a recession last?

A recession will last as long as economic activity is in decline, which can be as short as a couple of months or longer, sometimes lasting years. While we can't predict exactly when recessions will occur or how long they'll last, understanding the patterns helps you prepare and make informed decisions.

How do mortgage rates change in a recession?

During a recession, interest rates usually fall. This is because the Bank of England base rate, the rate of interest it charges other banks and building societies to borrow money, may be lowered. By lowering the base rate, the Bank is trying to stimulate the economy by making it easier to borrow money and access credit, which in turn should stimulate spending.

As the cost of borrowing is reduced, banks and building societies may also lower their own interest rates, too. This means mortgage rates should go down in a recession, making getting a mortgage or remortgaging more affordable. However, as ever, this isn’t guaranteed.

See what you could be offered today

When you complete your details online with Tembo, our unique smart decisioning technology will compare your eligibility to thousands of mortgage products in seconds. You’ll then be able to see all the ways you could get on the ladder, or remortgage.

Is a recession good for mortgage rates?

If you are looking to buy your first home or remortgage onto a new mortgage deal, a recession can be a good thing if it results in lower mortgage rates. Locking in a low interest rate during a recession can be a smart move. Not only will monthly costs be more affordable during a time of stretched budgets, but locking in for longer could allow you to benefit from a lower rate even when interest rates begin to rise again once the economy starts recovering.

Of course, recessions impact people differently, and while lower mortgage rates can help some buyers, they're not a solution for everyone facing financial challenges.

Read more: How long should I fix my mortgage for?

How does a recession affect my mortgage?

It depends on the kind of deal you have:

- Fixed-rate: Your monthly payment stays the same until the end of the fixed term. You only feel rate changes if you leave early (which could trigger an Early Repayment Charge) or when the deal ends.

- Variable or tracker: Payments usually fall if the Bank of England cuts the base rate, so your bill could drop in a recession.

- Remortgaging: Lower rates can save money, but weigh any exit fees before you switch. Our award-winning mortgage brokers can show the cost of staying put versus switching if you’re unsure. Find out more

- Lending rules: Lenders often tighten affordability checks during downturns, so approval can take longer.

Next up: How to get lower mortgage interest rates

You might like: What happens when my fixed-rate mortgage deal ends?

Should I pay off my mortgage in a recession?

Only if you still have a healthy cash buffer.

- Keep at least 3–6 months of living costs in an easy-access savings account first. Jobs are less secure in a recession.

- Most lenders let you overpay up to 10% of your mortgage balance each year without a fee. Bigger lump sums may trigger early repayment charges (ERCs).

- Compare savings rates with the interest you’d save on the mortgage.

If unsure, speak to a broker or financial adviser before making a lump-sum payment.

You might like: Should I pay off my mortgage early?

Make your money work harder with Tembo

If you’re building a safety net before overpaying your mortgage, or want to supercharge your house fund, explore our competitive savings accounts, including ISAs and easy-access options designed to help you grow your savings faster.

Do house prices fall in a recession?

It’s not guaranteed that house prices will fall in a recession; it can happen if demand for new houses drastically falls. If house prices don’t fall, they might slow down, meaning they won’t increase as quickly as before. This can make recession a tough time to move for homeowners looking to upsize, but for first-time buyers, it can be a good time to negotiate a lower house price.

Is it possible to get a mortgage during a recession?

Yes, it is possible to get a mortgage in a recession, but it can be more difficult. Mortgage lenders such as banks tend to tighten affordability criteria during a recession, which can make it harder to be approved for a loan. However, there are ways to boost your mortgage affordability to help you get on the ladder.

Plus, if interest rates and property prices fall, a recession can be a window of opportunity for those who can afford to get on the ladder. You could not only negotiate a reduced purchase price, but also lock in a low rate of interest, which will make your monthly repayments more affordable.

However, it’s important not to jump to a decision. Recessions can lead to redundancies and pay cuts. You don’t want to find yourself in a brand new home that you can’t afford to keep! It’s crucial to get expert advice from specialists like mortgage brokers before deciding whether to buy a home during a recession or not.

Start your journey to homeownership today

At Tembo, we specialise in helping buyers and remortgagers boost their mortgage affordability. On average, our customers boost their buying budget by £82,000. See what you could afford today.

What happens to savings rates during a recession?

Savings rates can move in the opposite direction to what many people expect during a recession. When the economy slows down, the Bank of England often lowers the base rate to encourage spending and borrowing. When this happens, banks and building societies may also reduce the interest rates they pay on savings accounts.

This means returns on easy-access savings accounts and some variable-rate accounts may fall during a recession. However, fixed-rate savings accounts can sometimes offer more stability, as they lock in an interest rate for a set period. This can be appealing if you want certainty about how much interest your savings will earn.

That said, savings still play a crucial role during uncertain economic periods. Having a financial buffer can help protect you against unexpected costs, job changes, or income disruptions.

Find the right savings account for your goal

Explore our range of competitive savings accounts, including our market-leading Lifetime ISA and easy-access options designed to help you grow your savings faster.